In April of 2007, Angelo Mozilo, founder, chairman, and CEO of the not-yet-infamous mortgage lender Countrywide Financial, opened his firm’s annual report with a letter addressing shareholders. Mozilo acknowledged that Countrywide had “faced many obstacles,” including credit concerns that were becoming “acute, most notably in the nonprime space.” But he reassured readers that Countrywide had limited their exposure, and that they had tightened their lending guidelines to stabilize loan performance. The accounting statements that followed confirmed this story. Smiling out at readers alongside his president and COO David Sambol, Mozilo assured them that Countrywide’s best days were still ahead.

A year earlier, Mozilo had e-mailed Sambol to describe his concerns about their growing subprime business in vastly different terms. He viewed Countrywide’s 100% loan-to-value mortgages as “the most dangerous product in existence,” explaining that there could be “nothing more toxic” to the company’s financial stability. Over the course of the year, he repeatedly called the mortgages “toxic” and “poisonous.” Countrywide was “flying blind” with no way to assess the real risk on their balance sheet. This story, of course, never made it into Countrywide’s quarterly or annual reports. Their boilerplate prose and optimistic accounting gave only a vague and distant sense of the danger facing Countrywide—danger sufficient to prompt Mozilo and Sambol to exercise options and sell millions of dollars of stock before its value plummeted.

To give an account of something is to tell a story about it, and to hold someone accountable is to make him responsible for that story. At Countrywide, executives used accounting to spin a story that distorted the truth and deceived shareholders. They told the public a vastly different story than they told each other. But account books tell stories even when their keepers are not trying to deceive. In the eighteenth and nineteenth centuries, individual men and women used accounting as a guide to navigate the increasingly complex world around them. Bookkeepers braided together words and numbers, sometimes following the recommendations in the latest textbooks, but also developing their own idiosyncratic notations for making sense of the world. They scrawled rough and ready calculations alongside precise and orderly balance statements, revealing their anxieties, preferences, and priorities along the way. Following them illuminates the daily drama of accounting as a narrative, contested search for understanding and control.

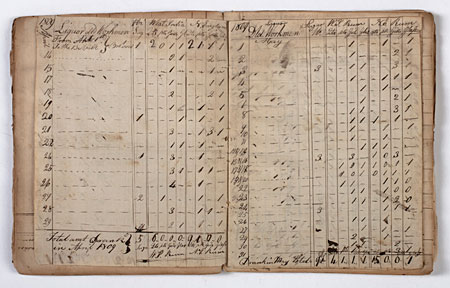

Documentation by Stephen Salisbury I, recording Laborers’ Consumption of Liquor. Pages dated April 1809 and May 1809 from account book by Stephen Salisbury I. Salisbury Family Papers, octavo, volume 23. Courtesy of the Manuscript Collection, American Antiquarian Society, Worcester, Massachusetts.

In 1828, Noah Webster’s dictionary defined “to cast accounts” as a lively, creative process. To “Cast accounts” was “to throw together several particulars to find the sum,” or even more vividly, “to throw together circumstances and facts to find the result; to compute; to reckon; to calculate.” In this mode, accounting was not an orderly process, but rather a vigorous and open-ended mixing and remixing of information. Students learned bookkeeping from textbooks and in schools, but they also felt their own way, experimenting with new methods to meet new needs. Account books offer a vivid display of this range of experimentation. Some are formal and precise, others jumbled and idiosyncratic, following a path that wanders like an inquisitive mind still unsure of its destination.

Keeping accounts was a daily quest for useful information. Sometimes quantitative information was punctuated by a bit of prose, verbalizing the intentions of a book’s keeper. In 1870, Thaddeus Fish of Kingston, Massachusetts, contemplated the buying and selling of eggs in his account book. He described how a woman had “bought 150 eggs of a country man.” She sold all of the eggs, but at an array of different prices, some yielding a profit, but others a loss. Fish, puzzling over her business, supplemented his muddled calculations with text: “I Demand to know whether she Lost or gained by her eggs.” The urgency of his demand reflected neither profit seeking nor an opposition to it. Rather it revealed the daily necessity of understanding whether time was well spent and which risks were worth taking.

“John W. Madden: Stationer, Printer and Lithographer, New Orleans, Jan. 8, 1815.” Bookseller label, Box 2, Range 4, Station B. Courtesy of the Bookseller Collection, American Antiquarian Society, Worcester, Massachusetts.

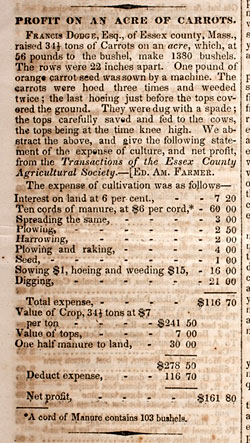

Individuals like Fish experimented with different ways of calculating profits and losses, assessments that were always ambiguous within the complexity of everyday life. Whether pigs were profitable stock, for example, was a subject of repeated consideration in British and American agricultural improvement magazines. Writers debated what should be included in their tallies of both costs and revenues. If pig feed was raised on the farm, for example, should it be charged to the pork account at cost or at its market price? What if it would have otherwise gone to waste? Still more elusive: How should a farmer account for that most priceless of pigs’ production—manure? And when his family finally enjoyed the pork, should he charge his account with the cost of raising the pig or with its price? Similar ambiguities arose for an array of other crops. When Francis Dodge tallied up his profits on an acre of carrots, he diligently accounted for a wide array of factors, including land and labor. He also deducted $60 for the expense of manure, but credited the crop with $7 for carrot tops, which he “carefully saved and fed to the cows.”

Visiting card inscribed with notation “Mrs. Salisbury requests the pleasure of…” with the rest of the card totally covered in ad hoc calculations, found between pages of a booklet with lists of investments of Stephen Salisbury I (probably estates), 1824-1831. Salisbury Family Papers, octavo, volume 32. Courtesy of the Manuscript Collection, American Antiquarian Society, Worcester, Massachusetts.

Bookkeepers even devised alternatives to systems that today appear obvious. The index was one of the first tools they adopted to help them grapple with the growing complexity and scale of commerce and manufacturing. Businessmen who traded with only a few partners had no need for an index, but as firms and factories grew, they needed new methods for quickly locating accounts. Today almost all indexes are alphabetical, but during the 1750s, the bookkeeper for the Newton family plantations in Barbados developed an alternative technique. He organized the accounts in the family’s slim ledgers in “AEIOU” order. Instead of classifying accounts by their first letter, he arranged them by their first vowel. This method had its drawbacks—it made uniform spelling imperative in an age of irregularity. But otherwise the first-vowel approach appears to have worked well. It met the main qualification for a system of indexing: every word included one and only one first vowel. Further, five categories fit nicely on a single page, conserving paper and easing indexing for the Newton family’s moderately sized plantations.

Balance sheet for “Profit on an Acre of Carrots,” taken from page 235 of The Soil of the South, Vol. II, No. 3, March 1852, Columbus, Georgia. Courtesy of the American Antiquarian Society, Worcester, Massachusetts.

The tabs on an index may not have radically influenced economic relationships, but other metrics and categories did. As the scale of American industry grew, the paper architecture of accounting often mapped directly to the brick-and-mortar architecture of the buildings and spaces. During the 1820s and 1830s, in the textile mills of Lowell, Massachusetts, and other New England towns, accounting enabled organization and coordination across increasingly large operations. Raw cotton entered at the bottom of the mills and rose through the factory where it was carded, dressed, spun, woven, and finally folded and cut for sale. The tasks of production were divided across the spaces of the mill, and overseers and clerks kept records in relation to these spaces. They calculated costs for labor, machinery, and raw materials by building and by room.

Bookkeeping transformed the rooms of the factory into profit centers. The spaces of the textile mills—from the spinning room to the lower, upper, and attic weaving room—became categories of profit and loss. Costs and revenues were allocated across these spaces, and overseers and operatives in each room became accountable to new measures, like cost per yard and cost per pound. Firm directors in Boston used these metrics to assess the performance of different stages of the production process. Without visiting the mill, they evaluated its efficiency, adjusting systems of supervision and monitoring wages. The categories of their account books structured social relations: with a different metric, success and failure would have been evaluated differently. Different men might have been promoted, hired, and fired. Accounting changed the allocation of credit and blame in both small ways and grand ones.

Because account books took time and money to maintain, they tell us what their users believed was most important and, more specifically, what they hoped to control. Before his death, Stephen Salisbury I kept extensive records relating to labor on their large farm. He tracked the number of days his men worked and how they were paid. He also documented the precise amounts of rum and sugar consumed by his workmen. Salisbury’s hand-lined tables included space to record liquor consumption in great detail: for each day, he noted who drank, how much was consumed, and whether it was New England Rum or West Indies Rum. Perhaps the family charged laborers for their drink and needed a record. More likely, Salisbury paid for the rum himself and monitored consumption to keep his workmen and his costs under control. Either way, workers drank a lot, and Salisbury found it necessary to record their alcohol intake—often in considerably more detail than he recorded their labor.

“Accomptants,” two pages of penmanship from a penmanship book by Samuel May of Leicester, Massachusetts, Copy Book, 1822, octavo, Volume “P,” No. 19 (1762-1856). Courtesy of the Penmanship Collection, American Antiquarian Society, Worcester, Massachusetts.

Textbooks applied the methods of accounting to an array of unconventional topics, including alcohol. Ira Mayhew’s popular textbook on practical bookkeeping remained in print from 1851 until almost the end of the century, reaching more than 140 editions. Mayhew offered a number of “exercises for practice,” one of which required students to calculate the costs of “fashionable tippling” at an interest rate of 7 percent. Students summed up the expenditures of a “Winebibber,” including cards, wine, and “kindred disbursements.” If they performed their calculations correctly, the results were striking: $6,529.29 for twelve years of such “social repast,” $19,504.22 for twenty-three years of the same, and a monumental $46,814.55 for thirty-four years of drunkenness. The narrative Mayhew constructed drew its data from a “reformed man” who had “squandered an immense patrimony.” It was designed to show students that immorality and indulgence risked financial ruin. Most of his exercises were more conventional—elsewhere readers could see the profits from a year of wheat farming, close the books for a general store, or witness the risk taken on by a speculator who ended in ruin. With these examples, as with the wine account, Mayhew encouraged his students to be diligent workers and good employees.

Textbook authors presented accounting as a practical and moral compass for navigating the world. Popular texts like Bryant’s and Mayhew’s promised that “the study and practice of Book-keeping would greatly promote the public good.” Bookkeepers ought to be diligent and honest, accounting a tool for accuracy and fairness. If each man accurately recorded his transactions, the “machinery of civil society would be thus more economically carried on,” and there would be “numerous checks” on the honesty and integrity of enterprise. In Mayhew’s view, those who criticized the methods of accounting were not just incompetent, but potentially evil. Drawing on biblical language, Mayhew accused these men of loving “darkness rather than light, because their deeds are evil, and [they] fear the light of correct entries, lest their deeds should be reproved.”

In another textbook published toward the end of the nineteenth century, Mayhew presented an even grander perspective on how accounting could help students understand the world. As he wrote, “times have changed.” The railroads “traversing our widely extended country” greatly multiplied “the buying, selling, and exchange of products,” as did “the telegraph, the telephone, and cheap postage.” This “easy interchange” of goods made “neighbors of persons hundreds and thousands of miles apart.” This new complexity made “the knowledge and practice of Book-keeping a necessity of the times.” He saw accounting as the antidote to complexity, emphasizing the potential of bookkeeping practices to help answer an array of social and economic questions. The practice of accounting could be used to make sense of all kinds of topics.

“Numeration,” a page taken from a penmanship book by Rebeckah Salisbury, of Boston, Massachusetts. Copy book, 1788, octavo, Volume “P,” No. 22 (1762-1856). Courtesy of the the Penmanship Collection, American Antiquarian Society, Worcester, Massachusetts.

Accountants’ lofty claims sometimes slipped into absurdity—Mayhew imbued bookkeeping with justice and virtue, rhapsodizing that those communities that embraced it would become “more fraternal and humane.” But within his extravagant prose was a kernel of truth. He understood that accounting was a powerful tool for understanding the growing complexity of the economy and that it provided ways to balance values—both moral and monetary. Further, he believed that everyone could put numbers to work, and that by doing so, men and women would negotiate more fairly. On the other hand, without widespread financial numeracy, he feared that the effects of accounting—both incidental and insidious—could be neither understood nor controlled.

“A Balance Chart, Exhibiting a Complete and Final Balance of the Accounts of a Merchant’s Leger Kept by Double or Single Entry. By James Bennett, Accountant.” Broadside (44 x 54 cm.), engraved (New York, s.n., 1836.) Courtesy of the Broadside Collection, American Antiquarian Society, Worcester, Massachusetts. Click to enlarge in a new window.

The keepers of nineteenth-century account books took great care to weave numbers into credible narratives. Consider the Salisbury family of Worcester, Massachusetts. In May of 1829, Stephen Salisbury I died after a prolonged illness. Shortly thereafter, his son, Stephen Salisbury II, began a new account book to prepare for the probate of the estate. Salisbury filled most of the book with lists and tallies of his father’s various holdings, but he began the volume with a narrative passage. Although he composed the opening in prose, Salisbury studded his sentences with numbers: “my beloved and honoured Father died aged 82 years, 7 months, and 17 days.” He had been “confined to this chamber for 6 days previous to his death,” the culmination of a infirmity that had extended “for the last 12 years.” In the final year of his illness he had “suffered less acute pain,” but for “the last 6 months he had frequent thirst and vomiting.” Despite the duration of the illness, Salisbury felt that his father had “breathed his last in peace,” his death resulting not from the violence of illness but from a “mere decay of physical power.” In this opening narrative, Salisbury took account not of his father’s finances, but of his life and the circumstances of his death. His enumeration blended utility and sentiment—as if counting and calculating could somehow grant him control over this most uncontrollable of events.

Bookkeeping held special significance for the elder Salisbury. Although he gave up many aspects of farm management, he continued to monitor his finances. Posting to his ledger provided him with the authority and control he had lost in other aspects of his life. As his son observed, during his final days, his father had done “much writing in his accounts,” almost fully posting “his Ledger to the month of his death.” Keeping accounts had given him the means to be productive despite his confinement, although he “confidently entertained” the expectation “that he should enjoy better health and the opportunity to be actively useful as in former days.”

The younger Stephen Salisbury crafted a persuasive narrative that verified the importance and authenticity of the accounts that followed. Despite “due examination and enquiry” the younger Salisbury never located “a last will,” and instead had to rely on his father’s account books and other financial papers. By attesting that his father’s “mind was clear and active to the last,” and that he continued to post his accounts, Salisbury assured readers of the accuracy and completeness of the document he was preparing. And, by noting that his father had expected to recover, he explained the lack of a will. For two generations of Salisburys, bookkeeping was both personal and practical. Through accounting, the elder Salisbury could confidently control his finances even as he lost control of his body. And his son, in preparing a final account of his father’s possessions, both secured his inheritance and narrated his respect for his beloved father.

The physical characteristics of nineteenth-century account books framed and verified the stories they contained. Some were large, leather bound, and embossed with gold, others small and stained from daily use. The book where Stephen Salisbury chronicled his father’s last days was moderately sized and of modest binding. The only clues to its importance are the many blank pages that followed the account—pages that would have been appropriated for other purposes in a less important book. Most of the other Salisbury account books are filled with calculations from cover to cover. Nineteenth-century bookkeepers used the space they had available, employing a variety of strategies to save the expense of paper. Instead of purchasing a new blank book, accountants often just flipped a used book over and began anew from the back cover. They completely covered scraps of paper in notes and numbers. Even book-bindings could become places for tallying up, with calculations squeezed into the small spaces where peeling leather had revealed a writeable surface.

Some bookkeepers decorated their work with elaborate off-hand flourishes, but textbook authors warned against the perils of over-embellishment. As Henry Beadman Bryant wrote in 1864, “it is a mistaken idea … that the ability to form a few wondrous curves in the execution of capital letters, or the adornment of a fancy title constitutes the chief qualification of a business writer.” Immodest flourishes were unlikely to impress practical men: they are “as much out of place on a page of business record, as a daub of oil color on a marble statue.” These preferences exemplified the ethics of accounting. Bookkeepers should be modest and meticulous, never excessive or extravagant. Neat, even penmanship was more important than decoration.

In 1844, accountant J.W. Wright submitted a question to the readers of Hunt’s Merchant’s Magazine. Wright described a series of transactions in which he took a loan, purchased cloth, went into business with a partner, and then dissolved the partnership. In his letter to Hunt’sWright requested guidance on how to close his books. In reply, he received forty-three communications, none of which solved the problem to his satisfaction. Even stranger, he exclaimed in a follow-up essay, “no two of your correspondents agree, either in details or aggregate results!” Eventually Wright received two replies that satisfied his needs, but he was convinced of the “lamentably deficient” state of accounting in America. Wright and other nineteenth-century bookkeepers believed accounting could be a true science, with right answers and wrong ones, but they encountered a man-made system, full of oddities and unevenness.

Wright might have been pleased by the state of accounting today. Under American law, all public companies must follow GAAP, the “Generally Accepted Accounting Principles,” a body of rules and guidelines jointly agreed upon by the American Institute of Certified Public Accountants (AICPA), the Financial Accounting Standards Board (FASB), and the Securities and Exchange Commission (SEC), which also serves as enforcer. In 2009, the various components of GAAP were authoritatively described in the FASB Codification. The print version fills four volumes and more than 1,000 pages, fitting a stereotype of accounting as dry, formulaic, and rule-bound.

But reading a modern annual report is not so different from picking up a nineteenth-century account book. Some are glossy, with full color pictures of smiling executives, today’s equivalent of elaborate flourishes and gilt binding. Others are simpler, printed in black on plain paper, displaying frugality in their stewardship of investments. All of them contain precise calculations but also pages of prose. In the wake of the financial crisis, there has been much discussion of how specific rules contributed to the intensity of the meltdown. Some of this discussion is certainly warranted—rules are important and must be carefully written. But it is a mistaken idea that rules can or should prevent accounting from telling stories. That accounting is a creative, narrative process is both a weakness and a great strength. Its narrative properties are essential for effective communication and also for rigorous questioning. The SEC’s case against Countrywide Financial is persuasive not because it highlights any one falsified calculation, but because it makes clear that the story executives told to the public was so fundamentally different from the stories they were telling each other.

Ira Mayhew believed that accounting was “necessary for every person engaged in the ordinary pursuits of life—for the day-laborer, the farmer, and the mechanic, as well as for professional men and persons engaged in mercantile pursuits.” Perhaps he and other nineteenth-century accountants were excessively optimistic about the potential of accounting as an all-encompassing tool in the search for order. But their belief that everyone could use and understand accounting has relevance for the present day. In an era when financial information seems increasingly the domain of experts, remembering that accounting is just a special way of telling stories makes it accessible to individual stockholders, consumers, and critics.

Further reading

The riveting, and remarkably accessible, case against Countrywide Financial can be found online at the SEC; The Salisbury family papers and an array of other early American account books are housed at the American Antiquarian Society. An evocative essay on the childhood accounting practices of Stephen Salisbury III, son and grandson of the Stephen Salisburys discussed here, appeared in Common-Place in July 2011. Particularly notable collections of business account books can be found at Harvard Business School’s Baker Library and the Hagley Library in Wilmington, Delaware. Selections from a number of interesting account books, including Thaddeus Fish’s, are reproduced in Winifred Rothenberg’s From Market-Places to a Market Economy (Chicago, 1992).

On systems of business information, see JoAnne Yates, Control through Communication (Baltimore, 1989), and Alfred Chandler’s classic, The Visible Hand (Cambridge, 1977). On counting and calculating more broadly, see Patricia Cohen’s A Calculating People (Chicago, 1982), on clerks see, Brian Luskey, On the Make (New York, 2010), and on the ideology of bookkeeping, see the work of Michael Zakim, including a recent essay in Common-Place. Bookkeeping as Ideology

The history of accounting also has a critical literature of its own, which can be found in a number of journals including Accounting, Organizations, and Society. For a survey of American accountancy, see Gary Previts and Barbara Merino, A History of Accountancy in the United States (Columbus, 1998).

This article originally appeared in issue 12.3 (April, 2012).

Caitlin Rosenthal is a doctoral candidate in the History of American Civilization at Harvard. Her dissertation explores the economic and social history of financial numeracy, tracing the development of quantitative reasoning in factories and on slave plantations. Caitlin became interested in the influence of numerical thinking while crunching numbers herself as a consultant with McKinsey & Company.

Even before the miniaturization of mokuks as souvenir items, these folded birchbark baskets served as trade items that also facilitated diplomacy between Native and colonial nations.

Understanding puzzles as agents of disorder runs counter to a common interpretation that associates puzzles with the quest for and ultimate affirmation of order.

“The life of a citizen,” they reminded the all-male jury, “lies in the hands of woman.” The result made prosecuting sexual assaults among acquaintances all but impossible.

Confederates’ quest for bones thus connects to a bizarre history of the use, and misuse, of human remains. Bones from the Bull Run battlefield were taken as acts of domination and displayed as trophies of war. However macabre, human remains became part of the deeply variegated material culture of war.

Morton and his skull measurements have long been part of the scholarship on American racism, but what happens when we draw Audubon into the racial drama?

Arnold’s unceasing efforts to elevate himself in society through marriage and professional work can be viewed through the lens of the houses he bought or built throughout his life.

Welcome to Commonplace,a destination for exploring and exchanging ideas about early American history and culture. A bit less formal than a scholarly journal, a bit more scholarly than a popular magazine, Commonplacespeaks—and listens—to scholars, museum curators, teachers, hobbyists, and just about anyone interested in American history before 1900. It is for all sorts of people to read about all sorts of things relating to early American life—from architecture to literature, from politics to parlor manners. It’s a place to find insightful analysis of early American history as it is discussed in scholarly literature, as it manifests on the evening news, as it is curated in museums, big and small; as it is performed in documentary and dramatic films and as it shows up in everyday life.

In addition to critical evaluations of books and websites (Reviews) and poetic research and fiction (Creative Writing), our articles explore material and visual culture (Objects); pedagogy, the writing of literary scholarship, and the historian’s craft (Teach); and diverse aspects of America’s past and its many peoples (Learn). For more great content, check out our other projects, (Just Teach One) and (Just Teach One African American Print).

How to cite Commonplace articles:

Author, “Title of Article,” Commonplace: the journal of early American life, date accessed, URL.

If you are looking for a specific Commonplace article from the back catalog and do not see it, or if have any other questions, please contact us directly. Please follow us on Twitter @Commonplacejrnl or Facebook @commonplacejournal and thank you for your support.